ICYMI: Market Intelligence at TD SYNNEX Public Sector’s Red, White and You

At this year’s Red, White and You conference, our market intelligence team detailed the ins and outs of what we’re seeing across the public sector. Throughout the sessions, one theme became clear: while success in the public sector market used to rely heavily on institutional knowledge and long-standing relationships, agency buying cycles, and slower opportunity development, the market this year looks different. It’s faster, calling for more efficiency, innovation and cost-optimization.

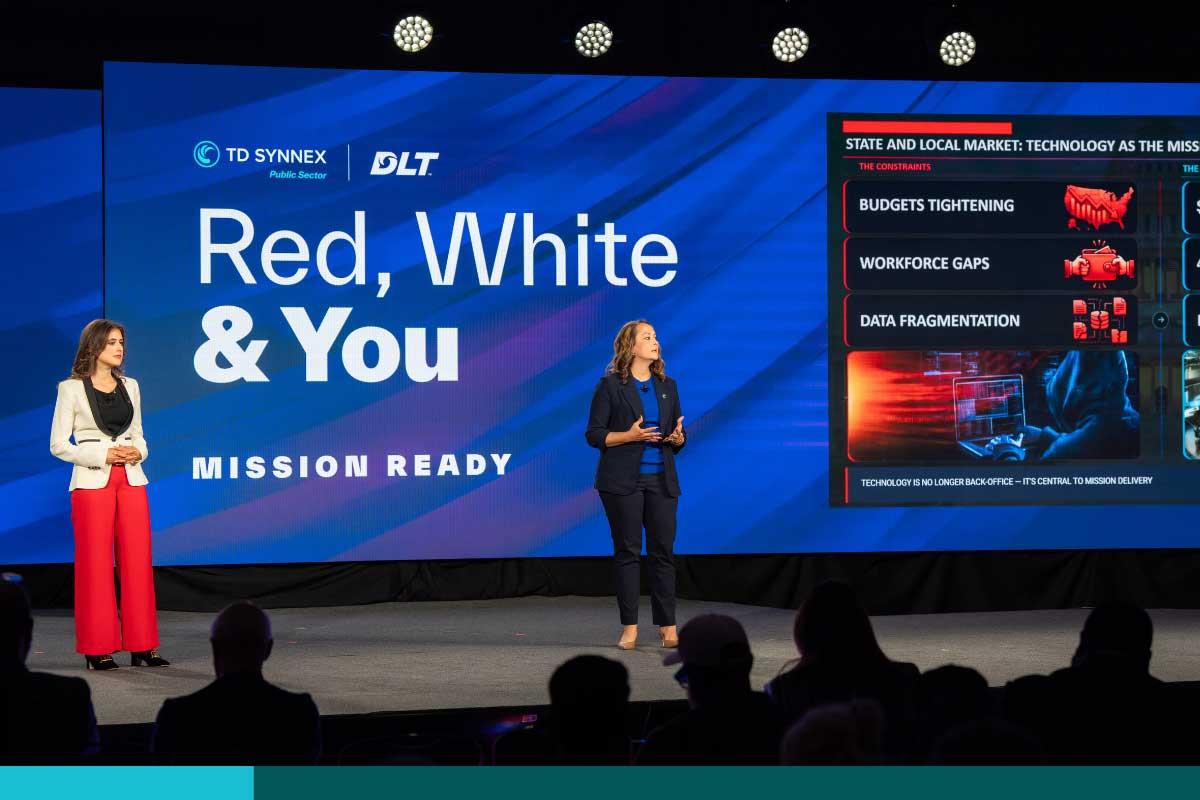

Across federal, state, and local government, agencies are operating under mounting pressure. Workforce shortages are affecting acquisition offices and operational teams alike. Budgets are tightening in some sectors while expanding rapidly in others. Longstanding contracts are being reevaluated, and agencies are under increasing pressure to modernize faster while delivering measurable results.

Beneath the disruption lies a much larger shift. Technology is no longer viewed as a supporting function within government. It has become central to mission delivery itself. Whether agencies are trying to improve cybersecurity, modernize infrastructure, manage workforce shortages, streamline citizen services, or deploy artificial intelligence responsibly, IT is increasingly positioned as the mechanism through which those outcomes are achieved.

That shift is creating significant opportunity for vendors and partners that can align solutions directly to operational and mission challenges rather than technology modernization alone.

The Big Themes: AI, Cybersecurity and Compliance

One of the clearest themes emerging across government is the rapid acceleration of artificial intelligence adoption. Last year, much of the conversation around AI centered on experimentation and future potential. Today, agencies are moving decisively into operational deployment. Federal agencies have now identified more than 3,500 AI use cases, while state legislatures introduced more than 1,000 AI-related bills in 2025 alone. At the state and local level, AI became NASCIO’s top technology priority for 2026, overtaking cybersecurity for the first time in more than a decade.

Importantly, agencies are no longer focused simply on whether they should use AI. The focus has shifted toward how AI can improve productivity, reduce administrative burdens, enhance decision-making, and help organizations do more with constrained resources.

Importantly, agencies are no longer focused simply on whether they should use AI. The focus has shifted toward how AI can improve productivity, reduce administrative burdens, enhance decision-making, and help organizations do more with constrained resources. State governments are already deploying AI to assist with document validation, workflow automation, analytics, permitting, procurement support, and citizen engagement. Federal agencies are embedding AI into cybersecurity operations, health research, fraud detection, and predictive analytics initiatives.

At the same time, agencies are recognizing that AI implementation is fundamentally dependent on data quality, governance, and integration. Across both federal and SLED markets, organizations are increasingly focused on connecting fragmented systems, improving interoperability, and strengthening data management practices. As a result, the opportunity for industry extends far beyond AI software itself. Demand is growing for cloud infrastructure, integration platforms, identity management, analytics tools, secure networking, and services that help agencies operationalize AI in a scalable and compliant manner.

Cybersecurity continues to remain one of the strongest and most resilient spending

Cybersecurity continues to remain one of the strongest and most resilient spending priorities across government. Defense agencies alone are requesting approximately $21 billion for cyberspace activities in FY2027, representing a roughly 36 percent increase over the prior year. Civilian agencies are also investing heavily in cyber modernization, particularly around zero trust, biometrics, infrastructure resilience, and identity protection. Meanwhile, state and local governments are increasingly being forced to strengthen their own cyber capabilities as federal support programs and grant funding become less certain.

This growing emphasis on security is also closely tied to compliance. Defense agencies continue preparing for CMMC enforcement, while states and localities are facing increased pressure around accessibility standards, privacy mandates, and cybersecurity maturity requirements. Agencies are looking for solutions that simplify these obligations and integrate cleanly into existing environments without adding operational complexity. That creates an advantage for vendors and partners that can deliver scalable, interoperable, and compliance-ready offerings rather than isolated point solutions.

Market Drivers

Federal

Within the defense market specifically, modernization priorities continue accelerating at an unprecedented pace. The proposed Department of War topline budget is approaching $1.5 trillion next fiscal year, with substantial investments tied to artificial intelligence, advanced networking, autonomous systems, cybersecurity, quantum computing, and next-generation command-and-control environments. The emphasis is also being placed increasingly on speed: speed of acquisition, speed of deployment, and speed of operational capability delivery. Agencies are prioritizing technologies that can integrate into enterprise environments quickly and support scalable, data-driven operations across domains.

State and Local

At the state and local level, the environment is more fiscally constrained, but technology demand remains strong. SLED IT spending is still projected to grow between 4 and 6 percent in 2026, reaching approximately $160 billion. What is changing is the way governments evaluate investments. Agencies are increasingly focused on long-term ROI, workforce efficiency, operational automation and risk reduction. Technology decisions are being tied directly to measurable outcomes, particularly in areas like healthcare, public safety, fraud prevention, eligibility modernization and citizen services.

Federal policy shifts are also reshaping demand across the SLED market. Changes to Medicaid administration, SNAP requirements, cybersecurity funding and AI governance are driving new requirements for system modernization, identity verification, compliance automation and cross-agency integration. For industry vendors and partners, this creates a critical window for engagement while many agencies are still defining requirements and shaping procurement strategies.

Education

Education markets are experiencing many of the same dynamics. Schools and universities are facing enrollment pressures, staffing shortages, and growing operational demands while simultaneously trying to modernize learning environments and digital infrastructure. AI adoption is accelerating within both K-12 and higher education, but conversations are increasingly centered on measurable instructional and operational outcomes rather than innovation alone. Districts are also placing greater emphasis on data privacy, cybersecurity, accessibility, and governance as they scale digital learning environments and AI-enabled services.

Across every sector, the broader market message is becoming increasingly clear: agencies are not simply buying technology. They are investing in operational resilience.

That reality is reshaping how vendors and partners position themselves in the market. Success this year depends less on standalone product capabilities and more on the ability to demonstrate how solutions integrate into agency ecosystems, reduce operational burdens, accelerate mission outcomes, and support long-term efficiency. Agencies want partners that understand the broader pressures they face and can help them modernize in ways that are scalable, secure and financially sustainable.

The vendors and channel partners best positioned for success will be those that recognize this moment not simply as a period of disruption, but as a transition toward a more integrated, AI-driven and outcome-focused government technology environment.

For even more intel targeting public sector trends, priorities and funding signals, visit our market intelligence hub.

Related Blog Posts